In mid-July, we reported that the United States Treasury is seeking public comment from the marketplace lending industry. As part of their request for information, there were 14 questions that were asked. Over the past few weeks here at Lend Academy and LendIt we have been compiling our responses and we filed them with the US Treasury yesterday which was the deadline.

In mid-July, we reported that the United States Treasury is seeking public comment from the marketplace lending industry. As part of their request for information, there were 14 questions that were asked. Over the past few weeks here at Lend Academy and LendIt we have been compiling our responses and we filed them with the US Treasury yesterday which was the deadline.

A total of 104 responses were received and most are available for viewing online. Pretty much all the major players in the industry submitted a response including Lending Club who did a full press release about it. Our responses are below. A word of warning, this is the longest post ever published on Lend Academy, at just under 7,000 words, so I also uploaded a PDF of our full response here.

Q1: There are many different models for online marketplace lending including platform lenders (also referred to as “peer-to-peer”), balance sheet lenders, and bank-affiliated lenders. In what ways should policymakers be thinking about market segmentation; and in what ways do different models raise different policy or regulatory concerns?

The term marketplace lending is too narrow and not inclusive of the innovation taking place in the lending category. For the purpose of this inquiry, we suggest using the term online lending since we believe that the Internet is the key driver of the innovation taking place in our industry. Marketplace lending is one category within online lending.

We run a global conference called LendIt, which is focused on the online lending industry, and we are in search of companies that have incorporated the Internet into their business models, resulting in improvements to traditional lending. The key is to find companies that have improved the traditional process and avoid companies that may have a website but have not improved the traditional model.

There are two different types of online lending models: marketplace lenders and balance sheet lenders. In some cases we see hybrids of the two models.

Marketplace Lenders

The very first online lender was Zopa in the UK, which launched in 2005 and was soon followed by Prosper in 2006, then Lending Club in 2007 in the US. Today, this model has been replicated by hundreds of companies all around the world. In the US we call it marketplace lending, in the UK they call it peer-to-peer lending, and in China they call it Internet Finance. The business model is an agency model that connects lenders (we use the terms lenders and investors interchangeably) and borrowers. These businesses typically include credit underwriting and loan servicing divisions in addition to traditional operating divisions.

They are compensated through a one-time loan origination fee paid by the borrower and, since they service the loans, they typically charge the investors an annual servicing fee.

In 2014 Lending Club and Prosper changed the way they referred to themselves from “ Peer-to-peer marketplaces” to “Marketplace lenders.” The issue was that p2p lending only refers to the retail market and these platforms are accessed by both retail and institutional investors. We estimate that the Lending Club and Prosper marketplaces are currently 75-80% institutional and 20-25% retail. It’s important to note that Prosper and Lending Club are the only platforms available for non-accredited investors.

The defining characteristic of a marketplace is that it connects a pool of investors with borrowers. Some marketplaces provide only whole loans to investors, these investors are typically institutions, and some provide a mixture of whole loans and fractional loans. In the latter case the primary investors are individuals with loans being funded by dozens or even hundreds of investors.

Balance Sheet Lenders

There are many online lenders that are balance sheet lenders. They may source borrowers in a similar way to the true marketplaces but they fund these loans from their own balance sheet.

Balance sheet lenders either use their own cash on hand (Paypal, Amazon, etc) or they secure a warehouse line of credit (Kabbage, CAN Capital, etc) or some other source of debt capital that is held on their own balance sheet. Once they secure a borrower, the money is funded immediately and the loan becomes an asset on their balance sheet.

With this kind of model platforms will typically earn money in the interest rate spread between the returns from the loans (net of any losses from defaults) and the cost of their credit facility. Some platforms charge an origination fee to borrowers, while some do not.

Balance sheet lenders often compete directly with marketplace lenders for borrowers and their acquisition strategies can be very similar. It is on the funding side of the equation where they differ.

Hybrids

Several balance sheet lenders have started marketplaces. The advantage of having a marketplace is it allows for a diversified investor base. Balance sheet lenders typically have a very small number (typically less then five) of institutions providing funding. When a balance sheet lender adds a marketplace they will bring on dozens of investors.

Some marketplaces hold loans on their own balance sheets. This is typically a small percentage of the loans but it can provide assurances, particularly for newer platforms, that they believe in their credit model enough to take loans on to their own balance sheet.

The revenue model for a hybrid lender will often have a mix of borrower origination fees and interest rate spread revenue.

Regulatory thoughts/concerns

Regulators should keep in mind that on the borrower side of the marketplace most platforms are working under the exact same regulations as banks. This is because most platforms partner with a bank to originate the loan. The bank will hold the loan on their balance sheet for a short time (less than a week) and then sell the loan to the marketplace.

With that said there are many things that regulators can focus on:

- Lending Club and Prosper have to register each loan with the SEC as a security. This is a cumbersome and wasteful process that benefits nobody. Loans are being funded so quickly today that literally no one reads these filings.

- Non-accredited investors are excluded from participating in this asset class except people who live in certain states that have approved Lending Club and/or Prosper.

- Regulators should be concerned about the maintenance of a level playing field between individual and institutional investors. So far, there have been no incidences of any investors being given preferential treatment but this is one area that concerns some investors.

- Most platforms don’t offer investing to retail customers due to regulations that make it cost prohibitive.

- Platforms will often service the loans themselves. Strong standards are needed to be in compliance with all debt collection laws.

- Backup servicing should be mandatory for all platforms who do their own servicing. This will reduce platform risk for investors.

- We would like to see greater access to this asset class for non-accredited and retail investors, since it is a relatively safe and appealing fixed income product that could be included in retirement accounts. It provides access to capital to underserved borrowers, it empowers the investor, and it strengthens the fabric of the US society. From the platform’s perspective, it diversifies the investor base, which provides for increased stability.

We believe that the trend will continue to shift from Balance Sheet to Marketplaces and we hope that the trend shifts from an environment that is dominated by institutional investors to a balance with retail investors. We would like to see policy and regulation focus on opening this market to retail investors, similar to the other two major online lending markets in the world: UK and China.

Q2: According to a survey by the National Small Business Association, 85 percent of small businesses purchase supplies online, 83 percent manage bank accounts online, 82 percent maintain their own website, 72 percent pay bills online, and 41 percent use tablets for their businesses. Small businesses are also increasingly using online bookkeeping and operations management tools. As such, there is now an unprecedented amount of online data available on the activities of these small businesses. What role are electronic data sources playing in enabling marketplace lending? For instance, how do they affect traditionally manual processes or evaluation of identity, fraud, and credit risk for lenders? Are there new opportunities or risks arising from these data?based processes relative to those used in traditional lending?

These platforms have created the technology to make an online loan from start to finish a possibility. It also has made loan origination a much more efficient process resulting in funds being posted to a borrowers account in just a few days or even quicker. There are several ways that big data and technology are impacting marketplace lending today.

Loan underwriting

Technology, big data and the transparency of that data is one of the major reasons this industry has been a success. By using big data, lenders are able to create linear regression models and machine-learning algorithms in conjunction with their own credit models to better underwrite their customers. They use many of the same data points that traditional lenders use but they have also added new data sources. And as the marketplaces have exponentially increased loan volume, over time they have been able to improve underwriting and better price risk based on this data. This better underwriting and increasingly longer track record has resulted in lower rates for borrowers, while still continuing to attract new investors.

One of the true innovations that marketplace lending has brought are the new data sets that until very recently were not considered in traditional underwriting. Platforms can connect with the APIs from all kinds of companies in real time: ADP for payroll information to verify income, Yodlee for personal finances, Facebook or Twitter for identity verification. For small businesses the dataset is even more extensive: Quickbooks for financial data, UPS for shipping data, Yelp for review data, eBay, Amazon or Etsy for online store data and much more.

The biggest two marketplaces in the U.S. update their loan data quarterly, and at least with Lending Club potential investors are able to download this data. Although they have restricted some fields to lessen the ability of competitors to reverse engineer their credit models, this transparency is what gave new investors the confidence to invest in this new asset class from the very beginning. Other marketplaces will offer their loan data under an NDA to potential institutional investors.

Fraud Detection

With no face-to-face interaction it is critically important for platforms to have sophisticated fraud detection. Many of the same data sets that are used in loan underwriting are optimized specifically for fraud detection with a borrower’s online footprint being carefully validated. For most platforms any borrower that does not pass all the automated fraud detection tests will be flagged and investigated manually. Although at least one company in the small business space, Kabbage, has a 100% automated underwriting process with no human intervention and has succeeded in keeping fraud to a tiny fraction of their loan book.

These advances in online fraud detection have resulted in a surprisingly low rate of fraud at most platforms.

Borrower acquisition

In this new age of data borrowers can be targeted much more intelligently than ever before. While marketplace lending platforms use traditional media such as television, radio and direct mail to attract borrowers they are increasingly using partnerships with lead generation companies to send them pre-vetted borrowers.

On the consumer side the two leading providers are Credit Karma and LendingTree and on the small business side there is Lendio, Fundera, Biz2Credit, and Connect Lending. These lead generation companies will select the best platform based on the criteria the prospective borrower enters. This leads to a very high percentage of borrowers obtaining loans from the online lenders thereby providing a much better customer experience.

Q3: How are online marketplace lenders designing their business models and products for different borrower segments, such as:?

- Small business and consumer borrowers;?

- Subprime borrowers;

- Borrowers who are “un?scoreable” or have no or thin files;

Depending on borrower needs (e.g., new small businesses, mature small businesses, consumers seeking to consolidate existing debt, consumers seeking to take out new credit) and other segmentations?

There are many market segments in online lending today:

1. Consumers

- Prime

- Near prime

- Sub prime

- Student

- Asset backed lending

- Auto (direct)

- Online pawn shops

- Healthcare

- Cosmetic & elective health

- Hospital services

2. Small businesses

- Long term

- Short term

- Merchant Cash Advance

- Accounts Receivable

- Point of Sale

- Equipment finance

- Asset backed lending

- Auto (indirect)

- Aviation

- Construction

3. Real Estate

- Short term bridge loans

- Buy to rent

- Non-qualifying mortgages

- Commercial

- Retail

Lending Club and Prosper focus on unsecured consumer loans for prime or near-prime borrowers. Their average borrower has a FICO of around 700 and, for the most part, they don’t accept borrowers with less than a score of 640. Since the inception of these lenders, there have been many new entrants who focus on different segments and now it seems there is a platform for every niche.

For borrowers who have a thin file there are some unique approaches being taken. A company like Upstart focuses on young borrowers who have recently graduated college. They collect additional data points including the college they attended, standardized test scores, and academic history. Using their unique algorithm, they try to determine the future earning potential of a borrower. They are looking to identify borrowers who will be considered prime in the future but who may not qualify for a loan today from traditional lenders.

Student lending is a unique subset of consumer lending. The platforms here have focused primarily on refinancing existing student loans. There is a “one-size fits all” approach to traditional student lending and many new graduates have excellent credit. These people are able to refinance their loan at a lower rate, particularly in the case of private student loans, saving students often tens of thousands of dollars. Like Upstart, platforms here such as SoFi and CommonBond look at future earning potential.

Small business lending requires a very different approach than consumer lending. In the case of very young companies the only option for lenders is to underwrite based primarily on the personal credit of the company owners. More established companies have the luxury of a financial track record and so the health of the business is the primary factor considered during the loan application.

There is a huge variety of loan products available today for small business owners. Not that long ago small businesses had two choices: a bank loan or fund their business on credit cards using their personal credit. Now, there are many different loan products available to small business owners. What is important for small business owners is considering the total cost of the loan. Transparent pricing is a real issue for small business lending because the products are often so different. This is why some platforms have grouped together to create the Small Business Borrowers Bill of Rights. More on that in the response to Question 11.

Online platforms for real estate lending (typically called real estate crowdfunding) have exploded in just the last 18 months. This industry barely existed three years ago and today there are over 100 platforms offering real estate loans. Most platforms focus on short-term loans of less than 12 months for small developers looking to do a “fix ‘n’ flip” where they purchase a home, do some renovations and then sell. Other kinds of loans, such as buy-to-rent and commercial real estate loans are becoming more common today.

Real estate is a unique asset class with a very different underwriting process to other types of lending. This is asset-backed lending so here the platform will assess the underlying asset as well as the borrower.

There is a mix of debt and equity platforms, many offer both types of investments. Almost all platforms only allow accredited or institutional investors and there is a usually a high minimum ($5,000 or $10,000) per loan.

Regulatory Thoughts

From an investor’s perspective, regulators should pay attention to style drift and credit underwriting standards. The marketplace lending platforms are incented to originate as many loans as possible, thereby generating fees, so it important to monitor that the types of loans for the stated strategy are the actual loans that are being originated. So far, Lending Club and Prosper have established best practices including platform transparency and making the historical loan data files available for download.

From a borrower’s perspective, all forms of lending are potentially exposed to online lending alternatives. It is very difficult to cut through the clutter to find trustworthy options. We were encouraged to see the creation of the Small Business Borrower’s Bill of Rights. We hope that this frameworks gain tractions in the small business category and we hope that similar frameworks emerge in other categories.

Q4. Is marketplace lending expanding access to credit to historically underserved market segments?

While many platforms focus primarily on providing a better option for people who can already get credit some are expanding access to credit for people who have been excluded until now.

Examples of some online lending platforms expanding access to credit:

- Upstart focusing on young people with a good education who are just starting out and have little or no credit history.

- Avant targets the “middle class” borrower who has fewer options than prime borrowers.

- Freedom Financial is an example of a company who works with borrowers who have had some financial distress, a group that most platforms ignore.

- Oportun, formerly Progresso Financiero, targets the Hispanic market, a notoriously underserved market by traditional financial services.

- LendUp helps sub-prime borrowers transition from payday lending through education and a system that will actually improve the borrowers credit score.

- Lenddo is establishing an alternative credit score for people without a credit score.

- Kiva Zip is an impact investment platform to help customers and brand ambassadors support their local business.

We are seeing the most innovative forms of inclusive finance emerge outside of the US, typically through the use of alternative sources of data including telco data, ecommerce data, search data, and social media data. China in particular has granted credit bureau licenses to the leading consumer Internet companies (Baidu, Alibaba, and Tencent) and we are seeing promising early results of combining alternative data with traditional credit data.

Q5: Describe the customer acquisition process for online marketplace lenders. What kinds of marketing channels are used to reach new customers? What kinds of partnerships do online marketplace lenders have with traditional financial institutions, community development financial institutions (CDFIs), or other types of businesses to reach new customers?

We covered some of this in question 2 but here is a more complete list of the kinds of marketing channels used by online marketplaces:

- Traditional advertising: television, radio and print, usually with a direct response component.

- Online: paid search, SEO (search engine optimization), display advertising, affiliate, social media

- Partnerships: largest referrers to marketplace lenders are Credit Karma and LendingTree. Banks and credit unions are also becoming an important source of borrowers for some platforms.

- Direct mail: many platforms start with this because it is very easy to target geographically and allows borrowers to receive a pre-approved loan offer.

- Email: all platforms utilize email extensively.

- Loan brokers: most prevalent in the small business and real estate spaces.

- Repeat customers: many customers will borrow a second or third time.

- Acquisitions: this has just started happening, platforms will buy a company because they have a desirable borrower pool.

There are some newer platforms focused on working directly with community banks and even some larger regional banks. This is expected to be a major growth area in the future as more banks partner with online lending platforms.

Of special mention is the Lending Club-Citi deal that was announced at LendIt in April. This is a mutually beneficial deal whereby Lending Club provided their service to Citi so that Citi could satisfy its CRA requirements. Lending Club enabled them to do this for borrowers who live in remote geographic areas for very little cost.

Regulatory Thoughts

We suggest that regulators pay particularly close attention to the lead generation category, which is on the front lines of borrower education and acquisition.

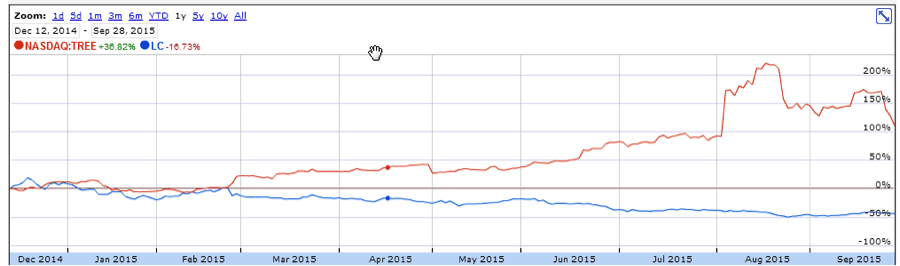

We believe that the stock price charts of Lending Club and LendingTree over the past year provide insight into the increasing value of customer acquisitions in the lending industry. LendingTree is a lead generation company and its stock us up 100% while Lending Club’s stock is down 50%. The lead gen companies are the downstream beneficiaries of customer acquisition dollars spent by the marketplaces. The investment community has recognized that the borrower community is the scarce commodity that can either constrain or drive the growth of a marketplace.

From a regulator’s perspective, the practices of the lead gen companies should be closely monitored. The marketplaces could pay increasing amounts per borrower lead as competition increases and their operations scale. The lead gen companies are incented to use aggressive tactics to acquire borrowers and should be closely watched.

Q6: How are borrowers assessed for their creditworthiness and repayment ability? How accurate are these models in predicting credit risk? How does the assessment of small?business borrowers differ from consumer borrowers? Does the borrower’s stated use of proceeds affect underwriting for the loan?

Every marketplace lending platform creates their own proprietary credit model based on their own analysis of credit bureau data. Most platforms hire experienced credit experts who have created these models at traditional lenders.

For those platforms with an established credit history these models have been very accurate in predicting credit risk. Large, sophisticated investors with a history of investing in consumer credit continue to invest in Lending Club, Prosper, SoFi and other platforms precisely because they have done a good job at evaluating risk.

The one proviso that we need to mention is that most of these platforms began after 2009 and so have not experienced an economic downturn. Lending Club, Prosper and OnDeck did all experience the economic downturn in 2008-09 and managed to come through ok although their loan books were much smaller then.

Small business underwriting is very different to consumer underwriting. Consumers are much more homogenous than small businesses. A group of borrowers with a 720 FICO score and a $75,000/year income will all tend to perform in a similar way. Every small business is different, even franchise businesses. So more data is needed to underwrite these businesses accurately.

Some platforms have begun to use borrower purpose to evaluate risk, although it is far from universal and results are not proven.?Most platforms, will not take loan purpose into consideration when underwriting a consumer loan.

Q7: Describe whether and how marketplace lending relies on services or relationships provided by traditional lending institutions or insured depository institutions. What steps have been taken toward regulatory compliance with the new lending model by the various industry participants throughout the lending process? What issues are raised with online marketplace lending across state lines? ?

Most platforms work with an FDIC insured institution to offer loans nationally. These banks will originate the loan and then hold on their balance sheet for a short time before selling to the platforms.

These banks, and there are only a small number of them, all work within the established regulatory framework. They undergo regular audits and internal reviews to ensure adherence to all applicable regulations. These banks assume most of the risk for monitoring the activities of the platforms as it relates to compliance and are subject to routine examinations.

While platforms could go state by state and apply for lending licenses themselves, most choose to partner with a bank that can then export the interest rate of that bank nationwide. Now, there is a case before the courts (Madden vs Midland) that is challenging the law for exporting interest rates across state lines and it will likely go to the Supreme Court so a final decision on this is not expected for quite some time.

One issue being raised by platforms is the burden of these state regulatory requirements that are often inconsistent with federal regulatory requirements.

Banks are also involved in the online lending process in other ways:

- On marketplaces, investor money is kept on deposit in a bank.

- For borrowers, loaned money is usually sent via ACH from the platforms bank to the borrowers bank account.

- Banks are partnering with platforms to obtain borrowers.

- Banks are buying loans on the platforms

- Securitizations, both rated and unrated, are underwritten by banks.

- Warehouse lines and leverage facilities for institutional investors are mostly provided by banks.

- Many employees at platforms come from traditional financial services.

Regulatory Thoughts

We are not the experts in bank compliance and regulation. We suggest that you pay particularly close attention to a few different constituents:

Cross River Bank: Cross River Bank has been the most active origination bank and is trying to instill best practices for our industry.

American Bankers Association: the ABA focuses on regulatory arbitrage, they want a level playing field where banks and non-bank lenders are regulated equally. They wrote this opinion piece after our LendIt Conference: “Banks Don’t Need Protection from Startups – But Consumers Sure Do.”

Title IV of the JOBS Act “Regulation A+”: Title IV of the JOBS Act recognized that the overhead of establishing and maintaining the regulatory framework for large public companies is too cumbersome for small business and it stifles access to capital and innovation. Reg A+ is a lightweight version of an IPO that provides a regulatory framework for smaller businesses. While focused on equity raises, Reg A+ is a good example of a two tier regulatory system for small and large companies.

P2PFA/FCA: In the UK, the P2P Financial Association is the industry association that created a regulatory framework that was ultimately adopted by the FCA. They classified P2P lending as a “lower risk” investment (more risk than bank deposits, less risk than equities). Their basic premise is that P2P lending offers significant economic and customer benefit, a regulatory framework is needed, but the framework must balance the benefits of innovation and efficiency against full consumer protection. We believe that the P2PFA/FCA solution is the best public-private regulatory approach to P2P lending in the world and we would support the implementation of a similar model in the US.

Q8: Describe how marketplace lenders manage operational practices such as loan servicing, fraud detection, credit reporting, and collections. How are these practices handled differently than by traditional lending institutions? What, if anything, do marketplace lenders outsource to third party service providers? Are there provisions for back-up services? ?

Loan servicing is done in house at many platforms. To satisfy investors these platforms typically also have backup servicers in place. These servicers can step in if there is ever a problem at the platforms.

Fraud detection is a major focus of all platforms. There are some very sophisticated automated systems that have been built to flag incidences of possible fraud.

Credit reporting and collections are done in a very similar way to traditional financial institutions. Collections are typically outsourced after a set period, often 30 days.

Regulatory Thoughts

What happens to the total cost of operations when delinquencies spike? How much of the operational efficiency of online lending is the direct result of underinvestment in their servicing and collections groups during a benign borrower delinquency period. The platforms say that they are fully prepared. Perhaps regulators could require a stress test or audit on platforms to ensure that they can scale their operations properly?

Q9: What roles, if any, can the federal government play to facilitate positive innovation in lending, such as making it easier for borrowers to share their own government-held data with lenders? What are the competitive advantages and, if any, disadvantages for non- banks and banks to participate in and grow in this market segment? How can policymakers address any disadvantages for each? How might changes in the credit environment affect online marketplace lenders?

There are many things the federal government can do to facilitate positive innovation in lending. We are at a critical time in history right now with lending going through a transformation, so it is crucial that the government acts thoughtfully and not stifle innovation. Other countries such as the United Kingdom and New Zealand already have sensible regulations in place that has been embraced by the platforms, the borrowers as well as large investors and these countries are attracting a lot of overseas capital because of that.

It should be pointed out that all marketplace lending platforms are heavily regulated already on both sides of their marketplaces. A myriad of federal fair credit laws already apply for borrowers and on the investor side federal securities laws apply to all platforms.

Having said that here are some thoughts on regulation:

- For any changes work with the marketplace lending community in a collaborative way to create a robust but welcoming environment for innovation.

- Work within, and help enhance, the current regulatory framework.

- Remove the necessity to file every loan with the SEC as a separate security for platforms who want to allow non-accredited investors.

- Foster partnerships with marketplace lending platforms and the banks, encouraging banks to offer the advantages that come with technology and product innovation.

- Help expand or facilitate the expansion of the secondary market to generate liquidity to market participants and loans to borrowers.

- Allow home state interest rates to be exported nationally.

- Allow more efficient access to IRS data for both consumers and small business.

- Expand the SBA budget to work with marketplace lending platforms as well as banks.

- Collect loan level data and apply it to FRED – give us aggregated and anonymized insight.

- We believe that online platforms:

- Provide access to capital to creditworthy borrowers, some of who do not have access to an alternative source of capital

- Provide a sense of empowerment for lenders who have made the choice to directly invest (and impact) the lives of others.

- Strengthen the fabric of our society by leveling the playing fields and providing lower cost access to capital to underserved categories.

- For any regulatory enhancements we should consider those premises so that regulation can further strengthen the industry.

The bottom line is this. The U.S. has always led the world in financial services. But lending money to consumer and small businesses is going through rapid changes right now and it is never going back to the way it was last century. For the U.S. to continue to lead the world of financial services in this century it needs a regulatory framework that will encourage innovation. Otherwise, countries like the United Kingdom and China will likely be the source of continued innovation.

Q10: Under the different models of marketplace lending, to what extent, if any, should platform or “peer-to-peer” lenders be required to have “skin in the game” for the loans they originate or underwrite in order to align interests with investors who have acquired debt of the marketplace lenders through the platforms? Under the different models, is there pooling of loans that raise issues of alignment with investors in the lenders’ debt obligations? How would the concept of risk retention apply in a non-securitization context for the different entities in the distribution chain, including those in which there is no pooling of loans? Should this concept of “risk retention” be the same for other types of syndicated or participated loans? ?

There is no consensus in the industry on this issue. It is often discussed as a criticism of some platforms that do not have skin in the game, that there is some misalignment of interests between the platform and the investor.

On the surface this seems like a valid point, particularly given what happened during the financial crisis. But we would argue that there is no misalignment of interests whether or not a platform has skin in the game. These loans are relatively short term, so within a matter of months investors can see how the loans are performing. If there is underperformance investors can and will choose to stop investing. When this happens the platforms will struggle whether or not they have skin in the game.

People have been arguing for years that as the industry scales there will be the temptation for platforms that do not have skin in the game to loosen their underwriting standards. Even as the largest platforms originate billions of dollars in loans we can see that they continue to maintain their credit standards and this loosening has not happened.

The platforms that do choose to invest in their own loans and hold them on their own balance sheet often use that as a selling point to investors. But it feels unnecessary to legislate skin in the game for all platforms.

Q11: Marketplace lending potentially offers significant benefits and value to borrowers, but what harms might online marketplace lending also present to consumers and small businesses? What privacy considerations, cybersecurity threats, consumer protection concerns, and other related risks might arise out of online marketplace lending? Do existing statutory and regulatory regimes adequately address these issues in the context of online marketplace lending?

Current regulations adequately protect the borrowers from risk, particular on the consumer side where platforms must adhere to the same lending laws as banks.

On the small business side more could be done to increase the transparency for small business borrowers. Much of the pricing and loan terms are difficult for business owners to understand and there is no easy way to compare costs between loan products. The industry has already created a Small Business Borrowers Bill of Rights that has been adopted widely so new regulation in this area would be premature.

This Bill of Rights, specifically for small business owners, is a very important step for this industry. Many of the largest small business lending platforms have signed on to this Bill of Rights, which has the following tenets:

- The Right to Transparent Pricing and Terms

- The Right to Non-Abusive Products

- The Right to Responsible Underwriting

- The Right to Fair Treatment from Brokers

- The Right to Inclusive Credit Access

- The Right to Fair Collection Practices

On the subject of risk there are many considerations:

- Privacy risks – we need to ensure that platforms are not sharing their data unlawfully.

- Cyber Security – any business that operates online has cyber security risk. We have seen some of the largest corporations in this country fall prey to hackers so this risk will always be there.

- Consumer protection concerns – the current regulatory framework is sufficient here.

- Underwriting risk – recession could see large increase in defaults. Related: pressure to grow could see platforms loosen standards.

- Bad actor risk – could be fraud or mismanagement at a newer platform.

Risk can never be completely legislated away. While the risks will continue existing regulations are sufficient for protecting consumers and small businesses.

We believe that the key to long term success here is three fold:

- Platforms should provide clarity on the terms for both the lender and the borrower

- Platforms should provide historical data files of all loans ever originated making as many variable as possible available to analyze

- Platforms should provide an open API for automated transactions

The best platforms will encourage the participation of the ecosystem. The creation of the ecosystem is the best path for success, since the ecosystem provides capital and innovation. If regulators were to push for platforms to increase transparency, provide historical data, and open electronically, the ecosystem will be enabled to filter for best and worst platforms.

Q12: What factors do investors consider when: (i) investing in notes funding loans being made through online marketplace lenders, (ii) doing business with particular entities, or (iii) determining the characteristics of the notes investors are willing to purchase? What are the operational arrangements? What are the various methods through which investors may finance online platform assets, including purchase of securities, and what are the advantages and disadvantages of using them? Who are the end investors? How prevalent is the use of financial leverage for investors? How is leverage typically obtained and deployed?

Marketplace lending began with individual investors at Lending Club and Prosper. Many early adopters invested despite the risks involved when these platforms were new. Today, many investors like to work only with established platforms that have a long track record.

Factors that investors consider when investing include:

- Interest rate

- Loan duration

- Creditworthiness of the borrower

- Loan purpose

- How quickly the available cash can be deployed

- Are there enough loans to create a diversified portfolio

- The minimum investment required per loan (for fractional loans)

The end investors fall into a number of different categories:

- Individual investors

- Family offices

- Hedge funds

- Publicly traded closed end funds

- Banks

- Insurance companies

- Sovereign wealth funds

- Pension funds

- Securitizations

- Endowments

- Some platforms operate their own funds.

- Financial advisors are starting to put their clients money to work.

Leverage is not a big part of the industry. While leverage is definitely used by some of the funds it is not a majority of the loan volume, in fact it probably represents less than 25% of the total loan volume. Leverage is obtained from banks such as Capital One, Silicon Valley Bank, Jefferies and many others.

Q13: What is the current availability of secondary liquidity for loan assets originated in this manner? What are the advantages and disadvantages of an active secondary market? Describe the efforts to develop such a market, including any hurdles (regulatory or otherwise). Is this market likely to grow and what advantages and disadvantages might a larger securitization market, including derivatives and benchmarks, present?

There has been a secondary market for retail investors for many years. It is a fully functioning and active market, particularly at Lending Club, with many individuals using it for liquidity just as it was intended. The problem is that only small investors participate, so institutional investors are left without this form of liquidity.

For institutional investors the only option that exists today is securitization. There have been more than a dozen securitizations done to date, mostly unrated, although some recent issuances have received investment grade ratings.

One of the challenges for a fully functioning secondary market for institutional investors is that it is not a high priority for most of the main players. The platforms have strong investor demand so they are reluctant to devote significant resources to help create it. Service providers who have the capability have other priorities as everyone tries to compete in a fast growing industry. Efforts have begun but they need buy-in from platforms.

The platforms question whether there will be enough demand today to create a sustainable secondary market for whole loans. Most loans issued are relatively short duration and for those investors that want liquidity they can get it by participating in a securitization.

There is no derivatives market yet but as the industry matures this will likely become a reality. Some investors do want the ability to hedge their positions in marketplace lending. Once indices/benchmarks develop then there will be those who want to go long and those short, and there are at least two companies working on providing that capability but this is still in the early stages.

Q14: What are other key trends and issues that policymakers should be monitoring as this market continues to develop?

One of the key trends that is happening today is the participation of banks in marketplace lending. Many banks see this as a way for them to deploy capital in a cost efficient way in asset classes that are complimentary to their existing holdings.

The recent acquisition of personal finance company, BillGuard, is also significant in that it shows that marketplace lending platforms want to provide more than just loans to their customers. They want to provide value added services to borrowers so that they can develop long lasting relationships with consumers. This is also happening on the small business side where some platforms offer free services to small business owners.

As we have mentioned previously, we also think that policymakers should be monitoring the regulatory environment in other countries, in particular the United Kingdom, where marketplace lending is thriving under a new regulatory environment.

There are several other things for policy makers to consider:

- How an interest rate rise will impact the industry.

- What happens during the next economic downturn.

- Are borrowers still being treated to fair pricing and transparent loan terms.

- Applying current regulation to changed product offerings

- Cybersecurity is of paramount importance to all participants

- Development of secondary markets