It is that time again when I share my investment returns. I like sharing these details because I believe in transparency and I know people are interested in my returns and how they are trending over time. I started out in marketplace lending many years ago with just Lending Club and Prosper but slowly have added new investments over the years. I included a relatively new account this quarter, StreetShares, they are a small business lender with a difference – you can read about them here and also listen to my podcast with the co-founders from last year.

Overall Marketplace Lending Return at 7.73%

The downward trend continues unabated in my returns. And while I said last quarter that was my worst ever, unfortunately I can now say the same again. In fact, this quarter set new lows, with one of my Lending Club accounts actually losing money during the quarter. This is the first time that has happened with any of my marketplace lending accounts.

I complained last quarter that the annualized return, based just on the latest quarterly numbers, on my main Lending Club account had dropped to 2.1% in Q4. Well, this quarter it dipped further. The balance on this account on December 31, 2016 was $39,733, the balance on March 31, 2017 was $39,472 for a -2.6% annualized return according to Lending Club’s own statements. I have had negative months here and there but never before have I experienced a negative quarter at Lending Club or Prosper since I started investing almost eight years ago.

When I look at where the recent defaults have been coming from the majority are in the D and E grade 36-month loans issued in 2015. These loan grades have underperformed significantly, something we covered in some depth earlier this year. When I said last quarter that I hoped the worst is behind us that clearly was not the case. I now expect my returns to continue to drift downward as more of this 2015 vintage hits their peak default months.

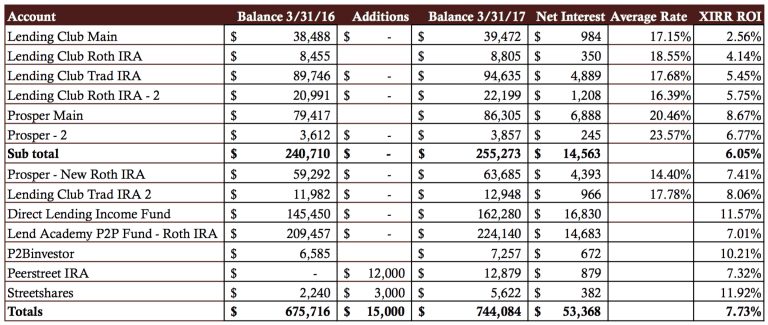

Now on to the numbers. Click the table below to see it at full size.

As you look at the above table you should take note of the following points:

- All the account totals and interest numbers are taken from my monthly statements that I download each month.

- The Net Interest column is the total interest earned plus late fees and recoveries less charge-offs.

- The Average Rate column shows the weighted average interest rate taken directly from Lending Club or Prosper.

- The XIRR ROI column shows my real world return for the trailing 12 months (TTM). I believe the XIRR method is the best way for individual investors to determine their actual return.

- The six older accounts have been separated out to provide a level of continuity with my previous updates.

- I do not take into account the impact of taxes.

Now, I will break down each of my investments from the above table grouped by company.

Lending Club

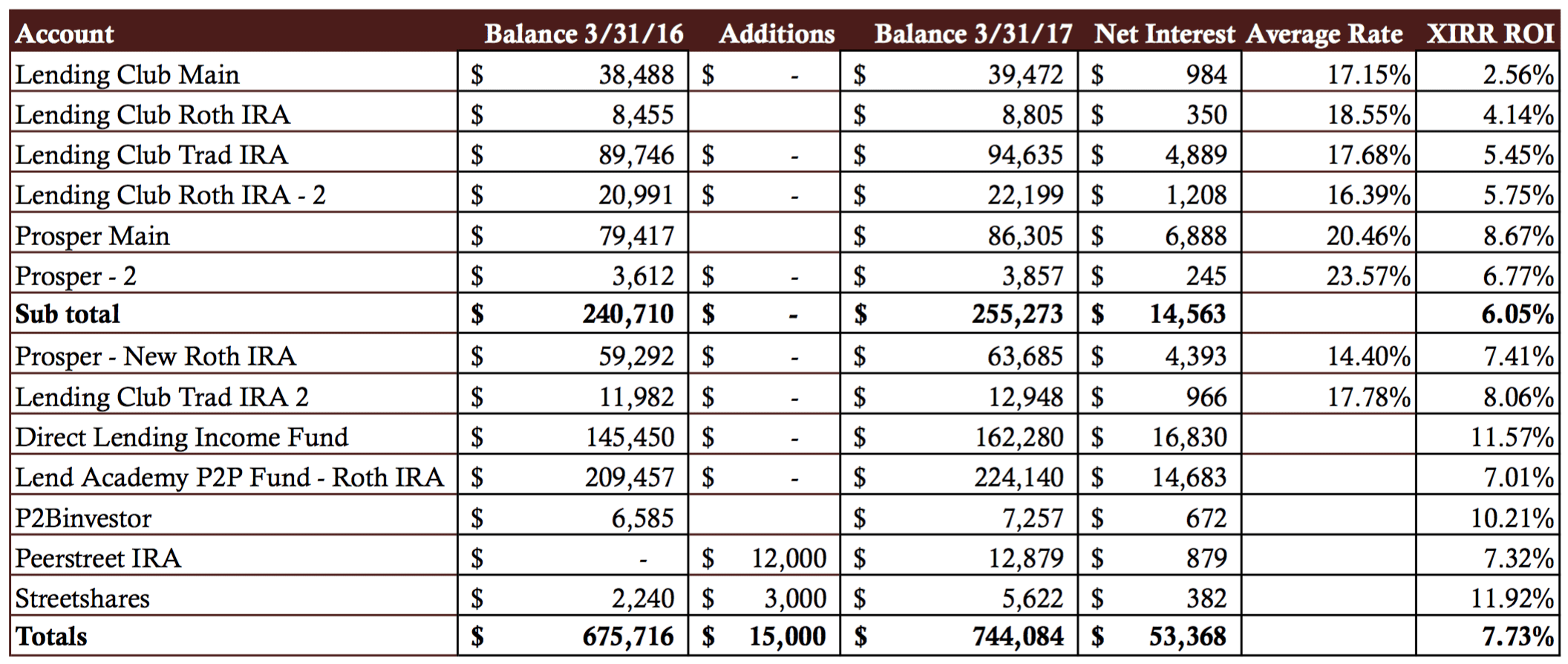

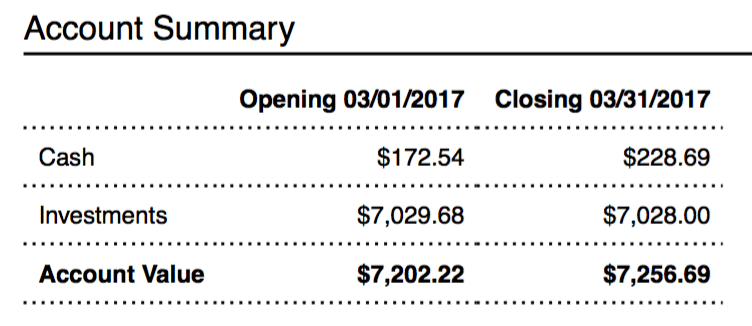

Above is a screenshot of what I call Lending Club Main – it was my very first Lending Club that I opened in June 2009. The first thing I want to point out here is the Net Annualized Return number that Lending Club provides. My TTM return according to my own calculations is 2.56% and Lending Club says my return is 8.32%. This is a pretty large delta and it comes from the fact that NAR looks at the total return over the life of each loan. Lending Club has a detailed explanation of how they calculate Net Annualized Return here. My best Lending Club account was my relatively new Traditional IRA which was opened in 2015 but all my established accounts, the youngest of which is six years old, were under 6%. I don’t expect much improvement in my returns in the short term because Q1 returns are going to be a drag on my TTM returns all year even if things start to get better.

Prosper

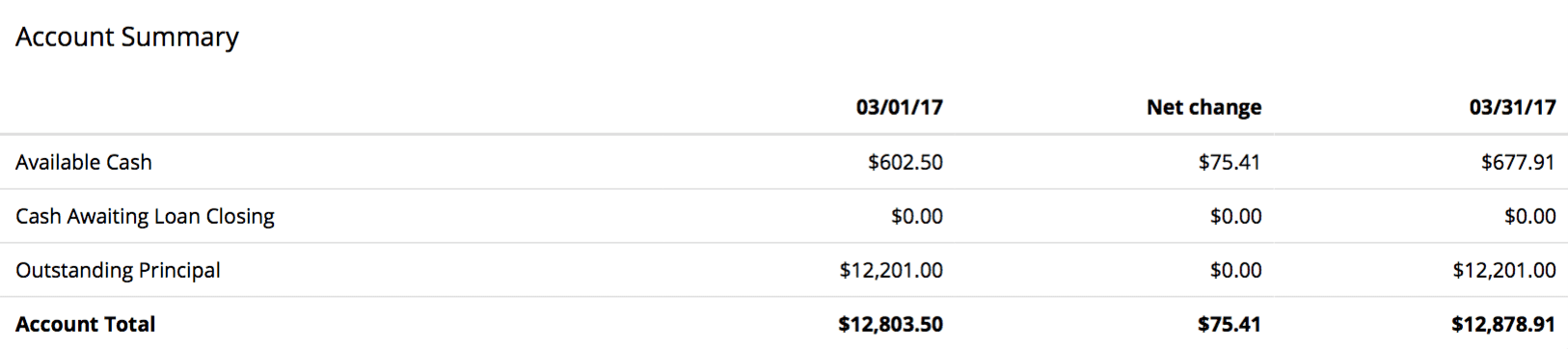

The reality is that during the last 12 months my Prosper accounts have held up reasonably well. In fact, my main Prosper account, that I opened in 2010, has been remarkably consistent over the past year – it has stayed in a tight range of between 8-9%. In the screenshot above you will see my Annualized Net Return says 13% but as we noted earlier this month Prosper made an error that resulted in a higher number being displayed here. This screenshot was taken at the end of March and now my return says 9.43% which interestingly is quite close to my actual return of 8.67%. However, my most consistent account is my New Roth IRA account that I opened in early 2014. It is my most conservative account of all my seven Lending Club and Prosper accounts with an average interest rate of 14.4%. My TTM returns here have ranged between 7.2% and 7.5% for over a year now.

Direct Lending Income Fund

Last month marked four years since I invested in the Direct Lending Investments fund. It has been my best performing investment by far over this time period. While yields have come down slightly from the initial 13-15% to 10-12% today I am still very happy with this investment. As the fund has grown, today it is closing in on $1 billion, it has changed focus from investing in high yield short-term small business loans to providing funding lines for a variety of consumer, small business and real estate lenders.

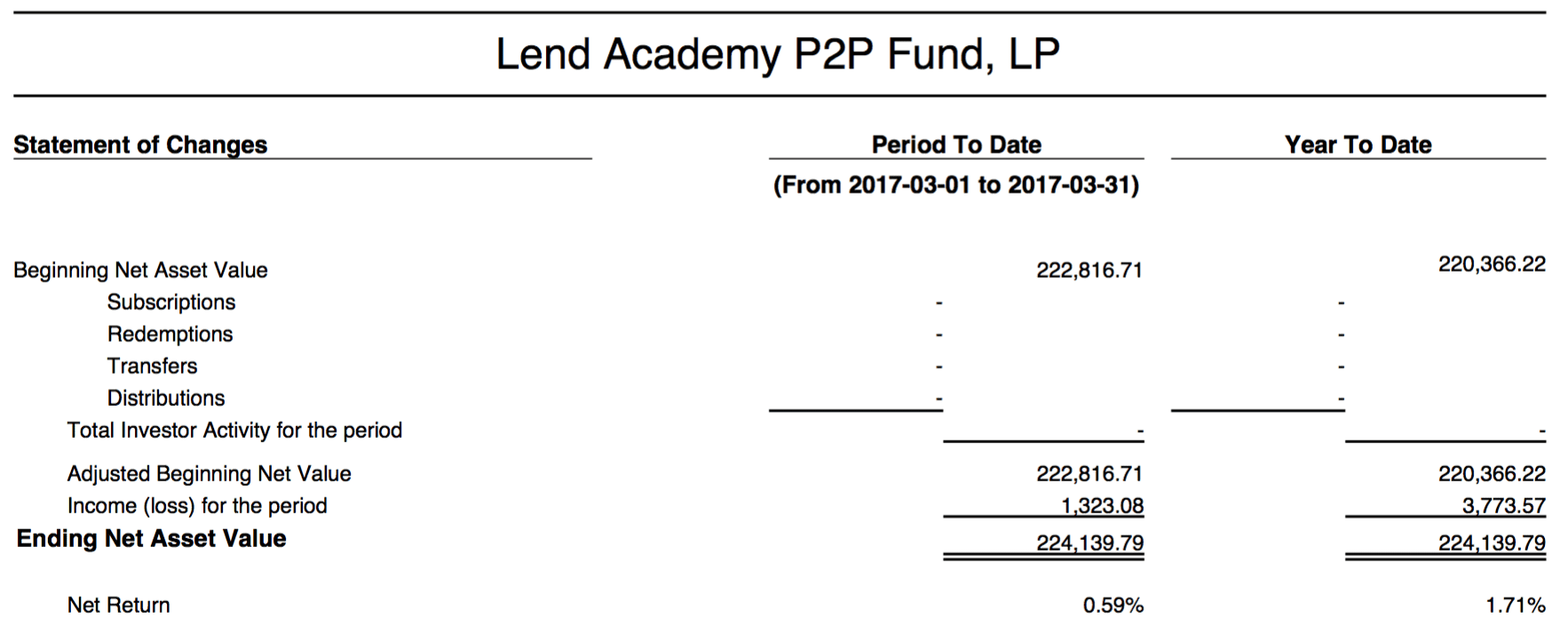

Lend Academy P2P Fund

The Lend Academy P2P fund is managed by the team at our sister company NSR Invest. It invests primarily in Lending Club and Prosper loans but also has investments in loans originated by small business lender Funding Circle as well as a small position in Upstart. While some of the funds in the industry have shown volatile performance in the last 12 months I am happy with the performance of this fund. It continues to do better than the Lending Club and Prosper accounts I manage myself.

P2Binvestor

P2Binvestor is an asset-backed working capital platform for small businesses that has been around for about three years. Full disclosure, I am on the advisory board of this company and have known the founders since before they began operations. What I like about P2Bi is that they provide a high yielding, liquid investment because the capital you are investing is backed by accounts receivable which has a quick payback. The big challenge they have today is finding new deals for investors. Many of the new deals coming on to the platform are filled up very quickly so it is difficult to stay fully invested. But I can’t argue with the performance – I have experienced consistent double digit returns for some time now.

PeerStreet

I opened my Peerstreet account about a year ago when I decided I needed to put money to work at the real estate platforms. As the consumer lending platforms have struggled I find real estate more and more compelling. The expected returns are similar but with the added advantage of having your investment backed by a hard asset. Peerstreet focuses on short term loans – typically 6-24 months with yield to investors in the mid to high single digits. I like the $1,000 minimum per investment at Peerstreet which has enabled me to feel comfortable starting with a relatively small investment. I have already almost cycled through my initial investment as 11 of my first 12 properties have already paid off in full.

Streetshares

As I said in my introduction my new entrant this quarter is Streetshares. I have liked their concept ever since I first heard about them back in 2014. They use an affinity model for marketplace lending where they focus on veteran-owned small businesses. I started investing in their loans soon after they launched and I put some more money in last December. While most of my portfolio is still quite young initial returns have been better than expected for the more mature loans in my portfolio. They are also one of the few companies that offer investment options for both accredited and non-accredited investors.

Final Thoughts

I feel like I have been a bit of a broken record on my updates over the last few quarters. For the past 12 quarters I have mostly seen a reduction in returns from the previous quarter. Three years ago my main Lending Club and Prosper accounts earned a combined 11.87% return, today I am at roughly half that. And during this same time unemployment has dropped from 6.7% down to 4.5%. What gives?

While I would be the first to admit now, looking back three years ago as investors we were being overcompensated for the risk we were taking. Lending Club and Prosper discovered that investors would accept lower returns which in turn allowed them to lower interest rates across the board to attract ever more borrowers. This would have been acceptable if defaults did not increase far more than expected.

I think it is clear today that in 2015 at Lending Club they became too aggressive in their underwriting. In a benign credit environment returns have gone down too far due to higher than expected defaults. This is what led to the pull back from institutional investors that began in Q4 of 2015 and really kicked in to gear in 2016.

The platforms have adjusted interest rates up several times over the last 18 months and I am confident that loans issued today will do far better than loans issued in 2015 assuming the economy keeps chugging along. Of course, that is a big if. The economic expansion is now getting on in years and we are overdue for a recession. This is why I am putting new money to work in real estate. While I continue to reinvest my money across the various platforms going forward, albeit in more conservative loans, for the foreseeable future new money invested through my IRA will be going into real estate platforms.

Finally, as I do every quarter I want to end by highlighting the net interest number which for the last 12 months stands at $53,368. While I realize a good chunk of this is taxable this is the real return on my investments. I am still several thousand dollars off my record of $56,960 that was set in Q4 of 2015. I am just hoping for some positive movement in this number as the year goes on.

As always feel free to share your thoughts in the comments below.