There is no industry standard when it comes to calculating returns on Lending Club and Prosper but this is something that is very important from an investors perspective. This is an updated post that we first covered in 2011 on different ways of calculating returns on Prosper and Lending Club. While both companies continue to provide returns in your account, there are some updates to what is provided by them and many people prefer other methods.

Here are six different ways for investors to get a handle on their returns.

1. Rely on Lending Club and Prosper

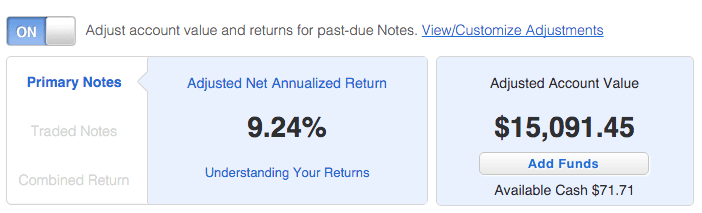

Both Lending Club and Prosper will give you their estimate of the return on your p2p lending portfolio. At Lending Club you are given the option to see your Net Annualized Return or your Adjusted Net Annualized Return. Lending Club breaks down returns into three categories: Primary Notes, Traded Notes and Combined return as shown below.

You can read more about the calculation Lending Club uses, but the major difference between net annualized return and adjusted net annualized return is that adjusted net annualized return takes into consideration loss assumptions based on loans that are in grace period, late or in default. This is their estimate of the return on the outstanding principal in your portfolio. Because they are only calculating returns based on outstanding principal, your returns may be overstated if you have idle cash in your account.

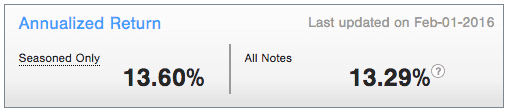

Prosper has a similar way of calculating returns, but instead of adjusted annualized returns they use a seasoned only number. Here is what they say about returns:

To calculate Annualized Returns, a total gain or loss is calculated by summing all loan payments received net of principal repayment, credit losses, and servicing costs. The gain or loss is then divided by the average daily amount of principal outstanding to get a simple rate of return. To annualize that rate, we divide it by the dollar-weighted average Note age of your portfolio (calculated in days) and then multiply it by 365.

Prosper breaks out returns on notes that have seasoned, meaning this number only uses those notes that are 10 months or older. These numbers are shown both on the overview and investing page.

2. The Simple Method

If you did not add to or withdraw from your account at Lending Club or Prosper then you can perform a simple calculation to calculate your ROI based on your balance on your monthly statement. You can do this for the latest month, quarter, year or any other period. For example, here are my numbers from Prosper for the third quarter of 2015. I did not add or subtract money from this account in that quarter.

Statement balance 6/30/15: $6,486.08

Statement balance 9/30/15: $6,710.33

Gain: $224.25

Then by performing this calculation: ($224.25/$6,486.08) * 4 you can find out your annualized ROI for last quarter. This computes to 13.8%, which is fairly close to Prosper’s estimate. The good thing about this method is that it does take cash into consideration since it is part of your account value.

3. NSR Platform Portfolio Analysis

The NSR Platform calculation is very similar to Lending Club’s adjusted net annualized return. The calculation is based off outstanding principal with notes being placed in separate buckets for grace period, each late status, default and chargeoffs. A loss factor is then assumed for each bucket based on historical data to calculate your ROI which is discounted by the expected loss rates. These assumptions can be altered for more optimistic or pessimistic projections. NSR’s calculation may differ slightly to Lending Club’s due to the lack of servicing fees provided in data exports

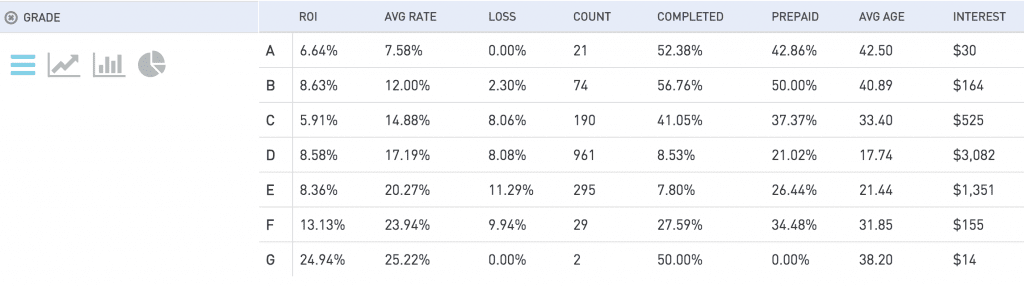

The benefits of using NSR to calculate your returns is that you can view the breakdown by any filter criteria which can help you better understand the breakdown of your returns. This is beneficial to determine which areas of your portfolio may be under or over-performing. For instance, in the below screenshot from NSR you can see that my D grade loans seem to be out-performing my E grade loans. I also need to take into consideration the average age of each grade and amount of notes, but this may make me reconsider my allocation to E loans.

4. XIRR() – Most investors preferred method

XIRR is the preferred way of computing p2p lending returns for many investors. Peter Renton, the Founder of Lend Academy uses this method to calculate his returns. By using the balances on your monthly statements and taking into account any withdrawals or deposits you can get an accurate picture of your ROI over any historical period.

The XIRR() function (it is explained well here) provides a way to calculate returns when you are adding or subtracting to your account regularly. It is simple to setup in a spreadsheet is an easy way to calculate a historical ROI number.

The XIRR() function (it is explained well here) provides a way to calculate returns when you are adding or subtracting to your account regularly. It is simple to setup in a spreadsheet is an easy way to calculate a historical ROI number.

The chart to the left is an example of how your own spreadsheet might look when calculating returns over 12 months. The initial balance is reported as a positive number and ending balance is always represented as a negative number. Contributions and withdrawals are listed as positive and negative numbers respectively. In the example to the left, there are only contributions, no withdrawals. These numbers should be inputted on the day the contribution or withdraw occurs.

The XIRR() calculation is a simple one. You have the dates in one column and the additions and withdrawals in the other column – this is the calculation for the spreadsheet above: =XIRR(B2:B14,A2:A14). XIRR is not perfect but it is the most accurate way to calculate ROI for any historical period.

XIRR has a few shortcomings. First, it doesn’t provide any guidance of ROI going forward. Second, no assumptions are made regarding status of notes, it is simply a calculation of money in, money out and ending balance. Finally, for new accounts it is likely to provide an inflated return due to fact that the notes haven’t seasoned. If you’re interested in calculating returns with XIRR, you can download our spreadsheet for free here.

5. Fair Value method of calculating investment returns

Although this method won’t apply to self directed investors, it is important to understand for investors who either invest or are considering to invest in a fund like the one offered to accredited investors from NSR Invest.

It is the most sophisticated method of measuring returns and has a deceptively simple name. It is called Fair Value. “This method is typically conducted by those practiced in the art of valuation,” says Bo Brustkern of NSR Invest, the General Partner of the Lend Academy P2P Fund.

Mr Brustkern’s fund uses the services of Arcstone Partners, a specialist valuation firm, to render a Fair Value of the fund’s assets for its monthly Net Asset Value (NAV) calculation. “It’s not for the faint of heart,” said Mr Brustkern, “because Fair Value valuation involves a note-by-note analysis involving thousands of positions, taking into account the contractual cash flows of each note, each note’s age and payment status, a discount rate that reflects current yields on comparable notes, and risk of default as of the valuation date.”

Fair Value attempts to deliver a more accurate NAV, which naturally means a more “fair” NAV for investors entering and exiting a fund. If there is a downside, it is that Fair Value also increases the volatility of fund returns. For example, the Lend Academy fund’s NAV reflected the change in rates at Lending Club and Prosper when each of these origination platforms raised rates. Since stability of returns is supposed to be one of the hallmarks of marketplace lending, the use of Fair Value is anything but uniform among funds in the industry. “When returns are lower because of external events our investors notice, and they are not always pleased” said Mr Brustkern. “Still, we stand by the fairness principle that underpins Fair Value calculations.”

6. LendingRobot’s Expected Return Calculation

LendingRobot recently announced a new way of calculating expected returns on a portfolio. I reached out to Emmanuel Marot, CEO and Co-Founder of LendingRobot to better understand this new calculation given that it is quite complex. If you’re interested in diving into the details you can read about it here.

Regarding their reasoning for this new calculation, Emmanuel stated:

Most of the loans investors have put money in are still on-going. Until they’ve reached maturity, have been repaid early or have defaulted, calculating their performance requires to predict how much they will keep paying. The reductionists may consider they will sum up to the outstanding principal, while optimists may believe all payments will be made on time, and pessimists may think it’s worth zero because it may default at any time. The truth is somewhere in between, and that’s precisely what LendingRobot aims to determine, based on typical loans characteristics

To explain it simply, Emmanuel provided this example highlighting the challenge that the current facts are not enough:

For instance, you invest $100 on a 13%, 36-months loan, that makes 3 net payments of $3.34. So the outstanding principal is now $93.07. What’s your return? (calculating ROI for the sake of simplicity, of course IRR would be more accurate):

- If you consider only the payments so far, your return is 3*3.34 / 100 – 1 = -99%

- If you add the outstanding principal, your return is (3*3.34 + 93.07) / 100 – 1 = 3%.

- If you add all the made and future payments, it’s (3 + 33) * 3.34 / 100 – 1 = 11%

In other words, to show current returns, you always need to predict the future payments or at least the value of the outstanding principal.

Conclusion

While most investors have their preferred method of calculating returns, it’s important to understand how returns are calculated on Lending Club and Prosper. If you’re interested in comparing your returns to other Lend Academy readers you can contribute to this forum thread.

What is your preferred way of calculating returns? Let us know in the comments below.