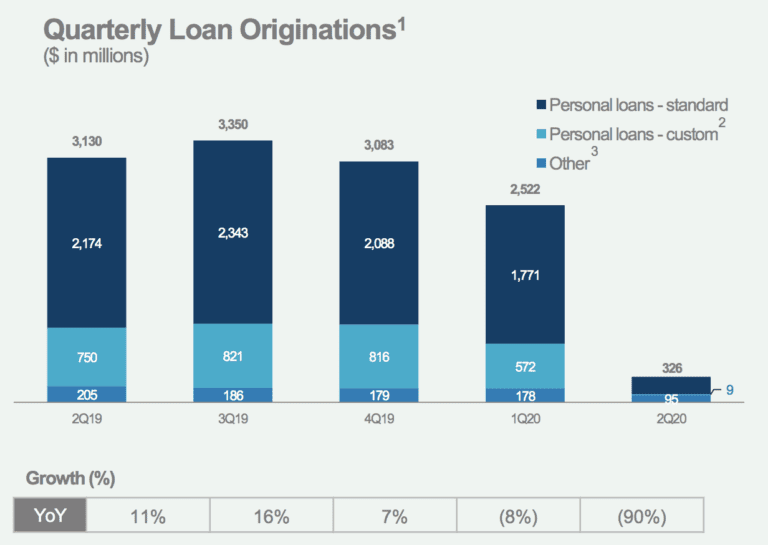

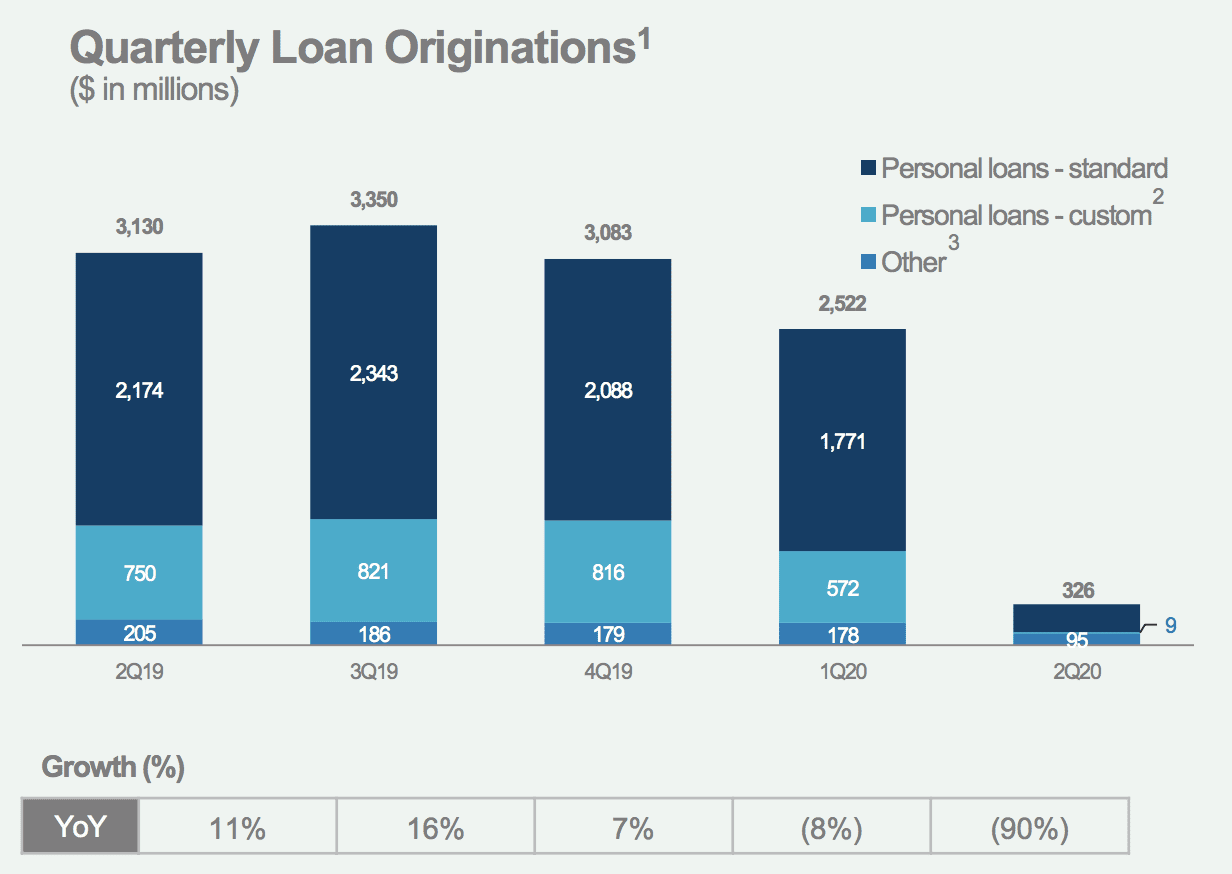

Today, LendingClub released their Q2 2020 earnings and as expected the results were pretty ugly. As the pandemic takes a big toll on the consumer lenders LendingClub’s origination numbers have dropped dramatically. To be fair, they did telegraph this in their Q1 2020 earnings call, saying that originations would be down 90% in Q2. Still, it was somewhat jarring to see the numbers in reality as demonstrated by the chart above.

LendingClub originated just $326 million in new loans in Q2, down from $2.5 billion in Q1 and $3.1 billion in Q2 2019. The last time originations were around that level was in Q1 of 2013 when they did $353 million in loans (I used to track the monthly loan originations at LendingClub before they were a public company).

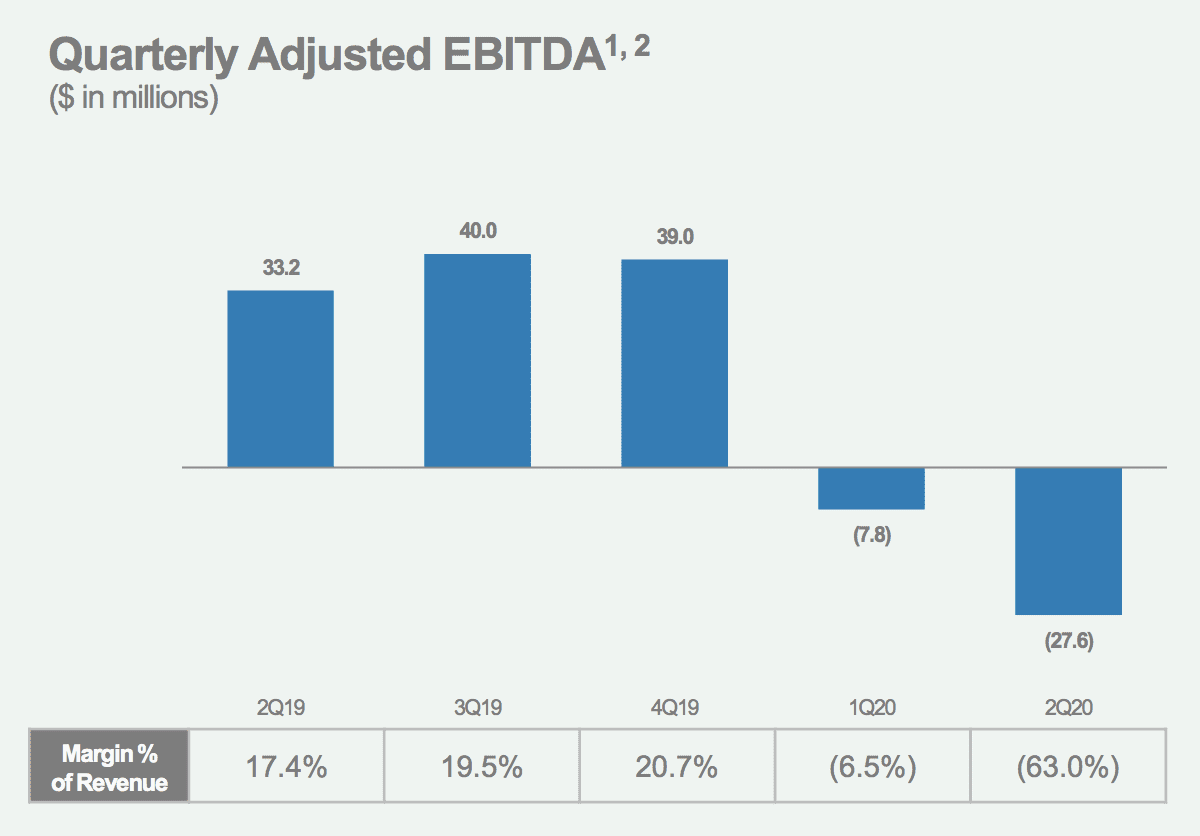

Not surprisingly, with such a big drop in originations, revenue was down precipitously and even though LendingClub reduced expenses significantly they still made a big loss based on adjusted EBITDA as you can see in the chart above. They made a $27.6 million loss on revenue of $43.9 million in Q2 compared to a $33.2 million profit on $190.8 million in revenue in Q2 2019. As I said, it was an ugly quarter.

On the earnings call this afternoon CEO Scott Sanborn said they are starting to see green shoots appear in their business. They have five of their top ten investors back on the platform albeit investing at much lower levels than six months ago. Each month has gotten progressively better since bottoming out in April and the expectation for Q3 is for originations in the $500 million to $600 million range.

Scott reported on the five guiding principles that he laid out for the company in the Q1 earnings call:

- Keep our employees safe – employees will will have the option to work from home at least through the end of the year.

- Preserve liquidity – they managed to maintain their net liquidity at $554 million, slightly up from the end of Q1.

- Protect investor returns – pre-COVID vintages are demonstrating resilience with an expected 3% return for recent vintages. Target returns are 5% going forward due to tightening of credit box.

- Support our members – payment deferrals are now below 5% after peaking at 12% in May with 66% of customers resuming full payment.

- Stay on track for the Radius acquisition – this is LendingClub’s number one strategic goal and they remain on track in their conversations with regulators.

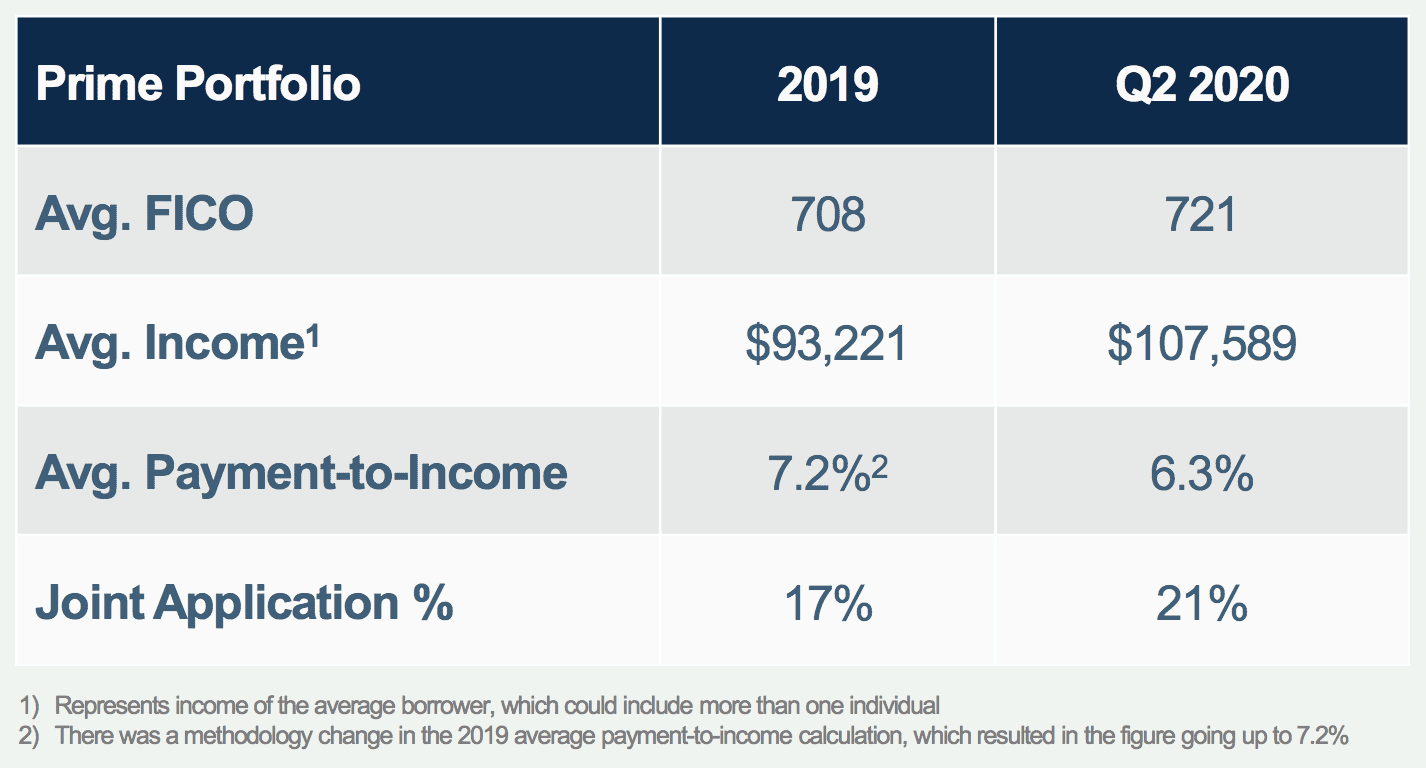

LendingClub tightened their borrower profile considerably as part of the 90% reduction in originations. They also focused on existing borrowers as they ceased almost all marketing activities. As you can see in this chart the average FICO went up, as did average income and the percentage of joint applications.

On the marketplace funding side you can see the dramatic shift in origination mix that occurred this quarter. Banks took more than two-thirds of the origination volume as many banks have stayed the course throughout the pandemic with their prime and super prime focus. And then the historically tiny self-directed investors, that has been the smallest category for years, jumped to the number two funding source. This is likely the result of many individual investors like myself who keep reinvesting in a hands-off, automated way.

You will also notice a big reduction in the LendingClub inventory as they conserved cash in Q2. They also sold several loan portfolios that they held on their balance sheet. They initially went to market with some higher yielding loans but moved to sell more prime loans as demand shifted during the quarter. They said they were very pleased in the interest from buyers and they ended up selling these portfolios for more than the expected.

My Take

This is a difficult time to be an unsecured consumer lender. I have been hearing from lenders across the board (with the exception of the buy now pay later space) and pretty much everyone is experiencing major challenges with reduced demand and a forced tightening of credit boxes.

While on the face of it these results look terrible the one piece that is most important right now is cash. LendingClub still has $564 million in cash and equivalents on their balance sheet which is not down that much from a year ago. They can withstand a prolonged downturn in their business.

It will likely take many quarters (hopefully not many years) to get back to pre-pandemic origination levels. But LendingClub seems to be making all the right moves to weather the storm. And next year they should add a digital bank to their offerings where they will be able to fund loans with cheap bank deposits. That will be when things get really interesting.