LendingPoint has made a name for themselves in the near-prime consumer lending space with an installment loan as well as a point of sale program (the latter through an acquisition). It has served them well as they have become one of the fastest growing companies in fintech. What many people may not know is that the leadership team at LendingPoint actually come from a small business lending background, having spent many years at CAN Capital or as it was known back then, Capital Access Network.

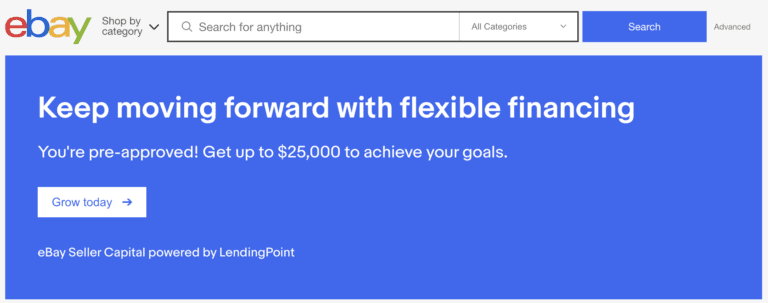

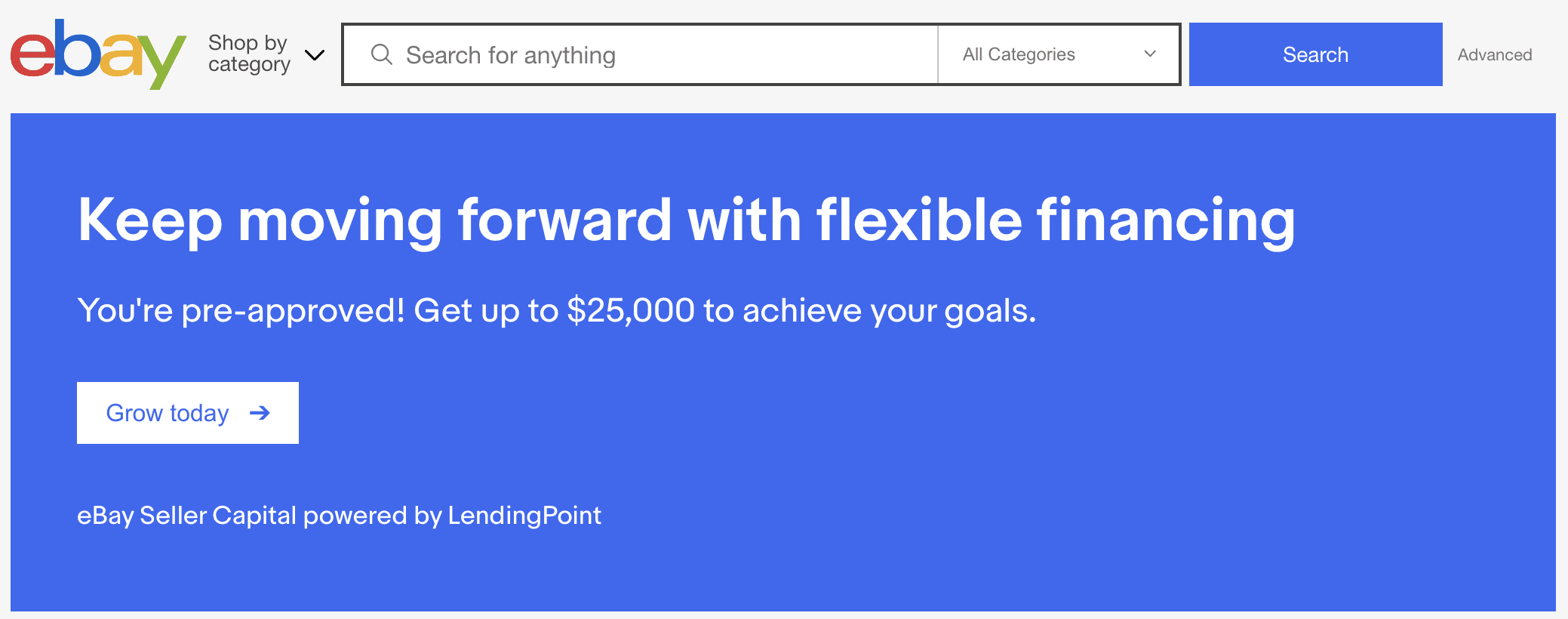

So, it shouldn’t come as much of a surprise that this consumer lender has added small business lending to its product mix. Today, LendingPoint and eBay have announced that they have teamed up to launch a new pilot program for eBay sellers called eBay Seller Capital, powered by LendingPoint. This new offering provides sellers with financing between $500 and $25,000 at rates ranging from 9.99% to 35.99% and loan terms up to 48 months. There will be no origination or prepayment fees.

I chatted with Tom Burnside, CEO and Co-founder of LendingPoint, yesterday to get the background on this deal. When I asked him why get into small business lending now he made it clear that LendingPoint is just following the flow of money. As the pandemic has taken hold the one area of the economy that is flourishing is ecommerce. They started talks with eBay six months ago and what really won them the deal was the level of automation that LendingPoint brings to the table. Tom mentioned this several times during our discussion that automation is so important for a good user experience and they have put a huge amount of effort into this at LendingPoint over the last couple of years.

The key to an automated lending decision is in access to data. With this program LendingPoint gets access to all the seller data so they can underwrite with a rich data set beyond credit data.

Here is what Tom said in the press release:

LendingPoint’s purpose is to accelerate and democratize commerce. We are thrilled to be able to use the data and technology we have built into our platform to help eBay sellers achieve their dreams. eBay sellers are some of the world’s most dynamic ecommerce players and our Loan Operating System will help them access the financial tools they need to achieve even greater success with their businesses.

Tom also pointed out that with their consumer lending program about 18% of their borrowers are using the money for their side hustle business. For a lot of eBay sellers they start off as a side hustle and with 25 million sellers the vast majority are still doing this part time. Even though it may be a part time business these entrepreneurs will need financing from time to time to buy inventory or expand their business.

When Tom and his co-founders started LendingPoint back in 2014 they decided to focus on near-prime consumer lending but the plan was never to stop just there. Tom said his vision all along has been to create what he calls the trilogy of lending: consumer lending, point of sale (they call it point of need) and small business lending. With this deal they have started to establish the third leg of this trilogy. While this is a pilot program the plan is to expand it in the fall to loans of up to $500,000.

My Take

I think the most interesting thing about this deal is that eBay decided to go with a company like LendingPoint with no real track record in the small business lending space. Sure, the management team have a deep history in small business lending but the company itself has little history here. There were certainly other companies that come to mind here such as Kabbage who actually started their business providing financing to eBay sellers. And they also have a high level of automation in their lending operation. Of course, eBay used to be part of PayPal and PayPal Working Capital would have been a logical fit but after their split in 2015 that was likely not an option.

That LendingPoint won the deals speaks to their track record and the higher profile they have established for themselves in the fintech lending space. They won this deal on their reputation and the technology they have built. But have no doubt about it this is a big deal for LendingPoint. While we don’t know the economics of the deal I am sure LendingPoint was quite aggressive in their approach here.

Few fintech companies globally have made successful moves across lending verticals. It will not be easy for LendingPoint but given their history and experience I will not be betting against them.