The regulatory context for cryptocurrencies continues to be vague, with many considering it a significant barrier to the mainstream development of the sector.

At the center of the issue for some jurisdictions (the U.S. specifically) is the definition of whether they are securities.

While much of the world has decided on its definitions, the SEC continues to grapple with the idea, caught in endless battles with Ripple and additional cases.

“One of the big questions is, why do we define this thing? It’s an emergent technology. It’s still being applied to the real world, so what’s the value of defining it?” said Mike Castiglione, Director of Regulatory Affairs for Digital Assets at Eventus. “The answer is to align incentives better so businesses can understand the rules.”

The year ahead could bring several defining conclusions on this matter, which could shape the crypto world as we know it.

Europe says, ‘No’

In late November 2022, Belgium’s Financial Services and Markets Authority (FSMA) made their conclusive announcement that bitcoin, ethereum, and other decentralized coins are not securities. The opinion was a result of the introduction of a “stepwise plan” applying a series of questions as to the token’s functionality to define them on a case-by-case basis.

Among other parameters, the report accompanying the announcement stated, “If there is no issuer, as in cases where a computer code creates instruments and this is not done in execution of an agreement between issuer and investor (for example, bitcoin or Ether), then in principle the Prospectus Regulation, the Prospectus Law and the MiFID rules of conduct do not apply.”

This does not leave the tokens exempt from all regulation, but it resolves a defining issue surrounding digital currencies that has the SEC stumped.

Belgium is one of many jurisdictions to come to a similar conclusion.

“In the Swiss law, you fundamentally have three types of currency,” said Yves Longchamp, Head of Research at SEBA Bank. “You have a payment token, you have utility tokens, and you have security tokens. We see all these layer one cryptocurrencies like bitcoin and ethereum are either payment tokens or utility tokens.”

He explained that to acquire this definition, the tokens are seen as currencies in a “digital country.” This extends to the introduction of staking (in the case of ethereum) as they are considered similar to bank deposits gaining interest.

“A lot of these definitions, whether commodity or security, hinge on whether someone has a right to the profits of an entity or profits of the company,” said Castiglione, commenting on the U.S. problem. “Another part is can you transfer it? Is there a secondary market in the crypto asset?”

“Additionally, whether something is a security or a commodity, there are rules about how you can treat investors, purchasers, or issuers in the marketplace. However, there are activities, irrespective of the definition, that are illegal and against regulations.”

The U.S.’s Ongoing Battle

Chairman of the SEC, Gary Gensler, among others, continues to debate the definition. On multiple occasions, the SEC has attempted to prove statements that various cryptocurrencies are securities. (Note: Gensler has admitted that bitcoin is not)

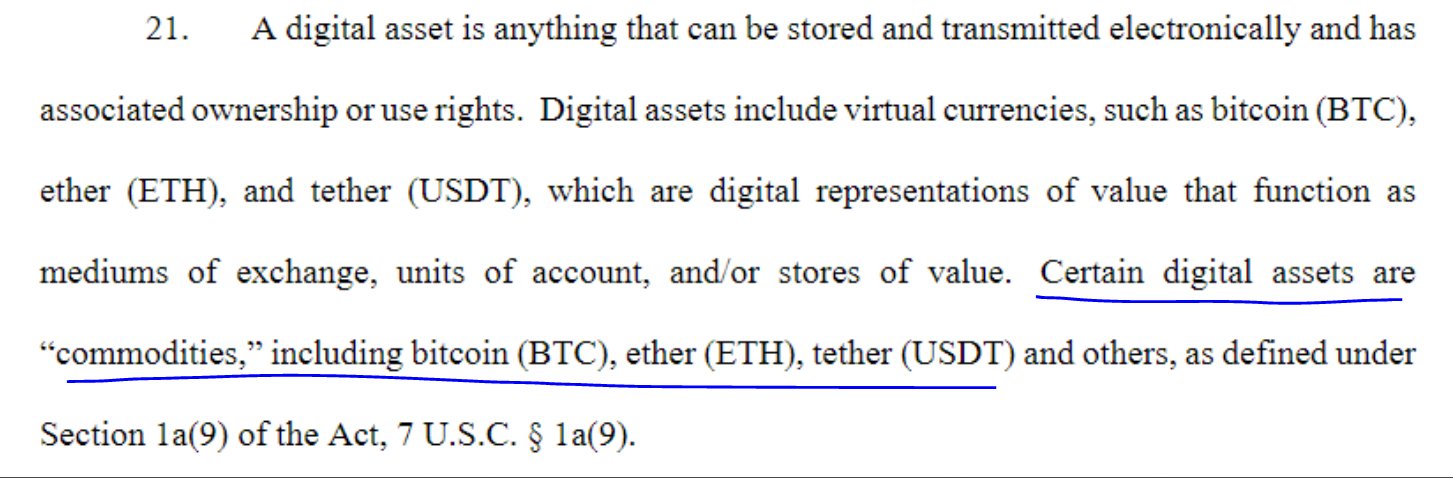

However, on Dec. 13, 2022, the Commodity Futures Trading Commission (CFTC) of the United States defined bitcoin, ethereum, and Tether, among others, definitively as commodities. This statement was included as part of the filing against FTX.

One would assume that this settles matters. Alas, this is not the case.

The thorn in everyone’s side

A conversation on the classification of cryptocurrencies would not be complete without a mention of Ripple.

The SEC has been caught in a seemingly endless battle following a case filed in December 2020 where they stated that Ripple was selling unregistered securities. A ruling is hoped to be passed in early 2023.

According to the SEC, on applying the Howey test to XRP, the coin could be considered a security. They have determined that the business, Ripple Labs, sold the tokens, and investment in the tokens would constitute an investment in a joint enterprise. Due to the marketing efforts and supply manipulation, investors could have expected the value of their investment to rise.

The case is significant because many consider the ruling to be definitive of a decision on the rest of the digital token industry. Regardless of the verdict, it could provide clarity on which others can base their model. However, many are concerned that an unfavorable ruling may constrict the development of the crypto industry.

The deadline for judgment is set for late January 2023.

Ethereum’s Merge created confusion

Before the CFTC’s statement, ethereum was also thrust into the SEC’s firing line due to their shift to a Proof of Stake consensus mechanism, an event titled “The Merge.”

“There seems to be an agreement that bitcoin is a commodity, therefore not a security. Why? Because we don’t know who the issuer is. It’s fully decentralized right now,” said Castiglione.

“On the other side, there seems to be an agreement that the ICOs, or initial coin offerings that you saw in 2017, are securities. There’s a regulatory mess that came with that because that looked like organized, defined entities issuing tokens to raise funds to develop their protocol and develop their business. So that looked very much like security.”

“Then there’s a theory from the SEC that a token can morph. It can start as a security. And then, if it’s sufficiently decentralized, it could lose this classification.”

A “security” stamp was staved off by apparent decentralization.

Ethereum, in its infancy, was wrapped up in the debate due to this ICO issue. The coin prevailed, but due to the Merge in September, their classification was brought back into question. The shift of consensus mechanism found much of the staking activity to reside within the US. This was used in an insider trading lawsuit against Ian Balina to define ethereum, once again, as a security.

RELATED: Merge happened; now what?

Ultimately the community has rejected this definition; however, it could mark a deficiency in the definition to date. The Howey test, traditionally used to make the determination, may not be up to the task given the blockchain development.

Where do we go now?

“There are many ways this can go,” said Castiglione.

“Scenario one is we muddle through still, which is doable but costly. If you don’t know whether there’s a referee on the field or what rules the referee will call, it’s just hard to operate with competence.”

“Scenario two is that all of this is adjudicated by the courts, so there is more precedent about how to define a crypto security versus commodity. But that can be lengthy and costly, and confrontational. The court option would probably come in response to an enforcement action that someone decides to fight.”

“Scenario three involves better definitions based on legislation. In the current environment, there’s consensus that any legislation should come with better definitions, and getting this right is a key element”.

Castiglione explained that both the Digital Commodities Exchange and the U.S. Token Taxonomy bill attempt to clarify this. He believes 2023 will bring a more structured approach that could assist the mainstream adoption of crypto.

“In the US, several bipartisan pieces of legislation will be reintroduced in early 2023. The main thrust is how to assign regulatory responsibilities between the Securities and Exchange Commission (SEC) and Commodities Futures Trading Commission (CFTC).”

“The core lesson is that regulation is coming. U.S.-based firms can rebuild trust by proactively being transparent and verifying they are following the hard-learned compliance lessons from other, non-crypto financial crises.”