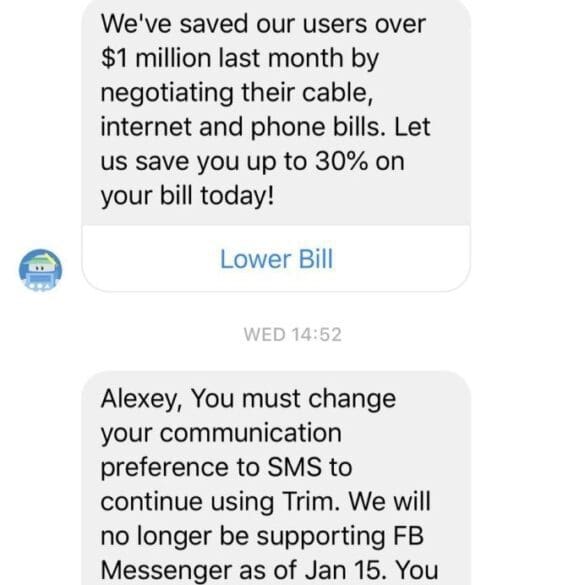

In the long take this week, I try out a contrarian point of view on personal finance chatbots. Trim, a savings chatbot, just withdrew support from Facebook Messenger. While lots of other chatbots are still invested in conversational banking, what could we take away from the counterfactual of chatbots failing to get B2C traction? What is the impact on the rest of the platform wars waged by Amazon, Google, and Tesla for connected homes, cars, and the Internet of Things?