The Center for Financial Inclusion at Accion (CFI) and the Institute of International Finance (IIF) in collaboration with the MetLife Foundation have released a report on financial inclusion; the report focuses on how partnerships between mainstream financial institutions and fintechs are expanding financial inclusion; findings are based on 24 in-depth interviews with firms and experts from around the world with emphasis on the emerging markets; the report is part of a two-year financial inclusion project from CFI, IIF and the MetLife Foundation called "Mainstreaming Financial Inclusion: Best Practices." Source

Financial inclusion is a factor considered by the Office of the Comptroller of the Currency (OCC) in all of its banking charters; American Banker discusses how the fintech charter's financial inclusion provisions compare to the Community Reinvestment Act requirements for banks; the new fintech charter would require fintechs to detail how they plan to promote financial inclusion with accountability from the OCC for those goals and more direct OCC enforcement actions for fintech companies. Source

According to a study done by the FDIC in 2015, about 25% of US households are underbanked, with about 8% being completely unbanked; according to the World Bank almost two billion people worldwide are still underbanked and access to the traditional banking system is minimal at best; the number is trending down as more fintech companies have arrived on the scene to offer financial products to these segments; these statistics have led a lot of companies to the conclusion that if you offer financial products via mobile devices these numbers will continue to trend downward. Source

PayPal CEO Dan Schulman is committed to helping support and promote financial inclusion by democratizing financial services and making banking activities more broadly available to everyone; the company is well positioned to support this initiative with more than six billion transactions occurring on its platform annually; Schulman provides some metrics around the benefits of digital transactions noting that the typical underserved population spends 10% of its disposable income on unnecessary fees and interest rates and with technology the cost of basic transactions can be lowered by as much as 80% to 90%.

While fintech innovation has greatly evolved in recent years, there is still much more to be accomplished; one area available for significant market growth is financial inclusion; Lend Academy talks about fintech innovation for the underserved bank customer in their article; LendIt will be running a financial inclusion track this year at LendIt USA to help support development of this market opportunity. Source

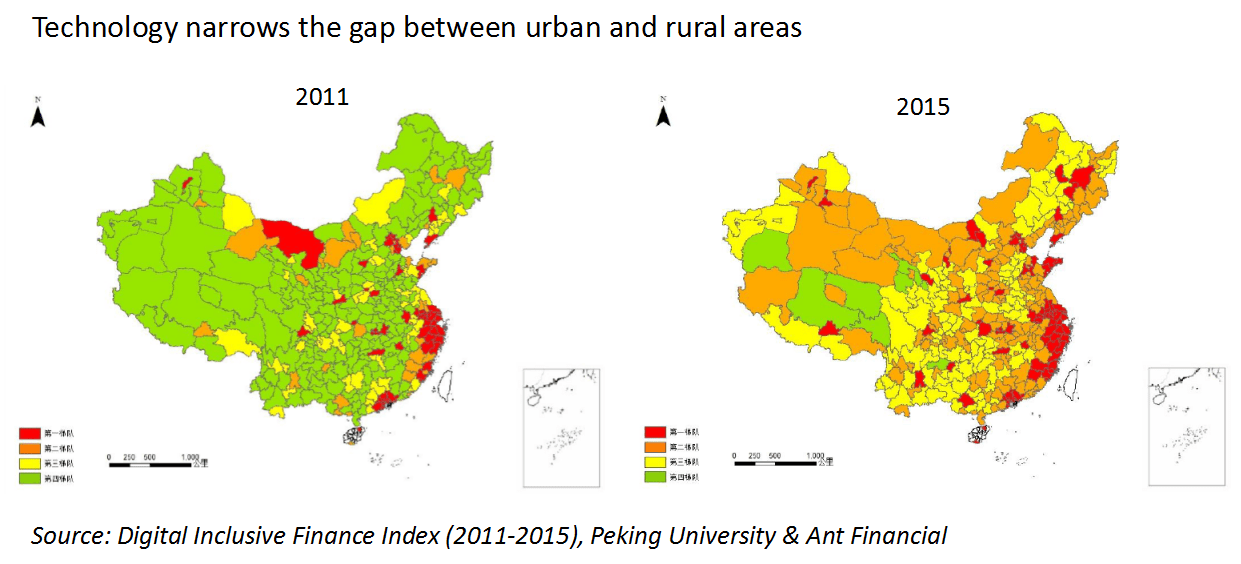

[Editor’s Note: This is a post from Sherry Zhang who is the latest member of the Lend Academy and LendIt...

Humaniq is a blockchain startup focused on financial inclusion; the company released an alpha version of their app; initial features include remittance payments and P2P lending as well as support for cryptocurrencies such as bitcoin and ether; Humaniq also has their own tokens called HMQ; app includes biometric ID verification for unlocking and verifying transactions; user profiles are based on facial and voice recognition algorithms; according to CEO Alex Fork: "Our initial target audience is people in emerging economies, and many of them don't have email. By using biometric ID we make the signup process more inclusive for people with low literacy while also lowering opportunities for fraud. Each real person will only ever be able to create one account, and no one will ever be able to steal their account. For businesses, a network full of real people is a dream come true, for reasons that are self-evident." Source

Fintech innovation is not only being fueled by faster, lower cost alternatives but also by the potential to reach a broader market demographic; while financial inclusion is a current market focus, many lenders have positioned their underwriting for the extreme opposite; American Banker's Penny Crosman analyzes both market extremes; notes the prevalence of current underwriting systems that integrate college degrees attained as a factor for credit approval resulting in a greater number of loans to elitist borrowers; identifies potential reform that could infuse financial inclusion mandates for all fintech companies beginning with provisions in the OCC's fintech charter that require financial inclusion considerations and following with further direction from the CFPB who is currently studying the use of alternative credit data for more inclusive borrowing; if financial inclusion mandates do become requirements it could provide even more momentum for the growing number of inclusive credit providers but also significantly upend a majority of the market's underwriting schemes which are based on algorithmic analysis with variables targeting socioeconomically elite borrowers. Source

Quona Capital has raised $141 million for its Accion Frontier Inclusion Fund focused on startups developing solutions for the underserved in emerging markets; investors in the $141 million funding round included Accion, MasterCard and JPMorgan Chase; other existing investors in the fund also include MetLife, TIAA Investments and the International Finance Corporation, a member of the World Bank Group; current Fund investments include Coins, Konfio and Creditas. Source

The fintech industry has come a long way in a short period of time. While financial technology has been around...